Insights into Delinquency Stages, Regulatory Realities, and Strategies to Maximize Cure Rates and Minimize REO Costs

Executive Summary

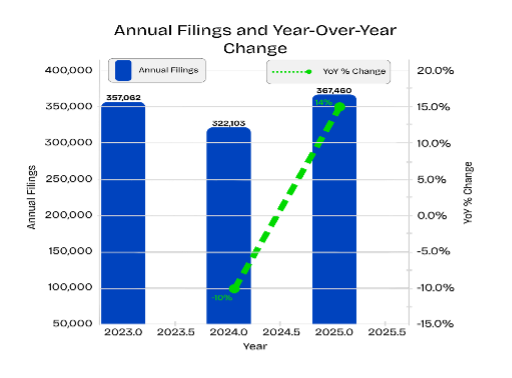

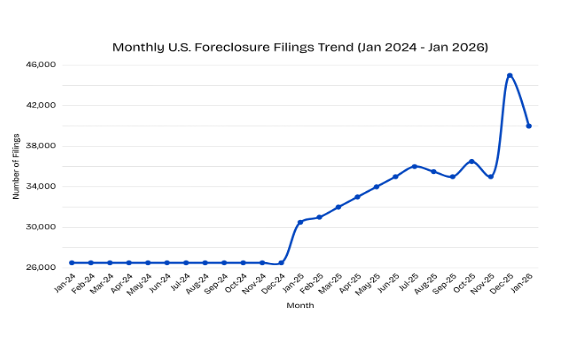

The U.S. mortgage servicing industry continues its gradual return to normalized foreclosure volumes after the historically low activity seen during the pandemic years. Data from ATTOM Data Solutions indicate that 367,460 properties nationwide experienced at least one foreclosure filing in 2025: Representing a 14% increase compared to 2024 and the highest annual total since the pandemic lows. This upward momentum carried into 2026, with ATTOM reporting 40,534 properties receiving foreclosure filings in January 2026 alone. That figure marked a 32% year-over-year increase and represented the eleventh consecutive month of annual growth in foreclosure activity.

Although current volumes remain substantially below pre-pandemic peaks (down approximately 87% from the 2010 high of nearly 2.9 million filings), the sustained increases reflect a market returning to more typical conditions. Primary drivers include the maturation of large loan portfolios originated inrecent years, rising property taxes and homeowners’ insurance premiums, and the full expiration of pandemic-era forbearance and borrower relief programs. While widespread home-price appreciation has built significant equity for many homeowners, providing a natural buffer against default progression, FHA-insured loans and specific origination vintages (2020, 2021) continue to show higher rates of delinquency progressing to later stages.

Federal regulatory requirements play a central role in shaping servicer behavior. Under the Consumer Financial Protection Bureau’s (CFPB) Regulation X, specifically §1024.41, servicers are prohibited from making the first notice or filing required to initiate a judicial or non-judicial foreclosure process until the borrower’s mortgage loan obligation is more than 120 days delinquent (with limited exceptions, such as due-on-sale clause violations or joining a superior lienholder’s action). This built-in pre-foreclosure review period is designed to prioritize loss mitigation options, including forbearance, repayment plans, loan modifications, short sales, and deeds-in-lieu (DIL), before legal foreclosure proceedings begin. Servicers must therefore balance strict compliance with these rules, ongoing borrower support obligations, operational cost control, and the need to protect investor recoveries.

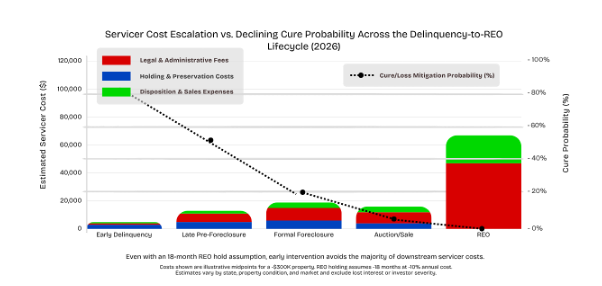

Proceeding deeper into the foreclosure process carries significant financial consequences for servicers and investors. Prorated annual holding and renovation expenses are commonly estimated in the range of 8–12% of property value (covering taxes, insurance, maintenance, utilities, marketing, and security), in addition to typical sales and closing costs of 5–7.5%. These expenses accumulate rapidly once a property reaches REO status, eroding net recoveries and tying up capital for extended periods.

In contrast, early and proactive loss mitigation produces materially better outcomes. Industry benchmarks from the Office of the Comptroller of the Currency (OCC) and historical mortgage performance data consistently show that the probability of successful cure or sustainable modification is highest when intervention occurs in the early delinquency window (0–90/120 days). Even after amodification is completed, re-default risk remains notable; older OCC Mortgage Metrics reports have documented re-default rates (60+ days delinquent) approaching or exceeding 25% within six months for certain cohorts, though more recent combination modifications in 2025 have continued to emphasize affordability improvements. Early engagement reduces the likelihood of progression to costly foreclosure and REO stages while preserving borrower homeownership where feasible.

This whitepaper provides a structured overview of the delinquency-to-disposition lifecycle, examines key regulatory considerations (including state-levelvariations such as California’s AB 2424), and demonstrates how integrated data-driven platforms and specialized services enable upstream interventions. By combining predictive analytics, borrower portals, timely valuations, property preservation, streamlined short-sale/DIL processing, and efficient REO disposition capabilities, servicers can meaningfully improve cure rates, reduce loss severity, lower operational expenses, and enhance overall portfolio performance in the 2026 market environment.

1. The Evolving Foreclosure Landscape in 2026

National Trends Foreclosure activity increased steadily throughout 2025 and continued its upward trajectory into early 2026, yet volumes remain far below the peaks experienced during the 2008–2010 housing crisis. The 2025 full-year total of 367,460 filings equated to roughly 0.26% of U.S. housing units, signaling a measured return to pre-pandemic market dynamics rather than a new crisis. January 2026 data reinforced this pattern, with filings rising 32% year-over-year for the eleventh straight month.

Regulatory Framework The CFPB’s Regulation X §1024.41 continues to anchor federal protections. Servicers may not initiate foreclosure proceedings until the loan is more than 120 daysdelinquent, creating a mandatory window for loss mitigation evaluation and borrower engagement. Dual-tracking limitations and requirements to evaluate complete loss mitigation applications further shape operational workflows.

State Variations and Procedural Delays Significant differences persist between judicial and non-judicial foreclosure states. Judicial states often experience extended timelines due to courtbacklogs and procedural requirements, while non-judicial states generally allow faster progression, though recent legislation has introduced additional borrower protections in some jurisdictions. In California, Assembly Bill 2424(effective January 1, 2025) added meaningful extensions in non-judicial processes: submission of a valid listing agreement with a licensed broker (at least five business days before the scheduled sale) triggers a mandatory 45-day postponement of the trustee’s sale. A subsequent bona fide purchase agreement can extend the timeline by another 45 days, creating up to 90 additional days for short sales or other resolutions.

Servicers navigating this landscape benefit from partners offering early delinquency detection, technology-enabled mitigation tools, and seamless end-to-end asset recovery solutions to maintain compliance while optimizing outcomes amid gradually rising volumes.

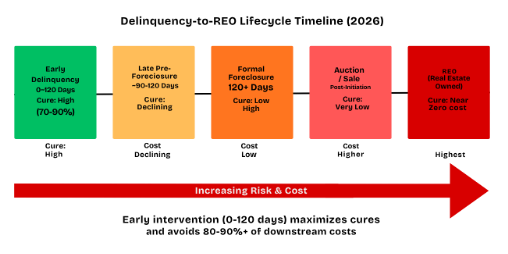

2. The Delinquency and Foreclosure Lifecycle: Stages and Timelines

Approximate timelines begin at the first missed payment (Day 0) and are influenced by state law, court conditions, borrower responsiveness, forbearance agreements, and legislative changes. Federal rules impose a minimum 120-day delinquency threshold before formal foreclosure initiation.

The table and associated lifecycle highlight why early intervention is critical: most successful cures occur before the 120-day mark, well before substantial costs accumulate.

3. Strategic Opportunities: Moving Upstream in Default Management

Maximum impact on cure rates and loss severity is achieved by shifting default management activities earlier in the cycle. Modern integrated platforms combinedata, technology, and operational services to support this transition from reactive foreclosure processing to proactive mitigation. Key capabilities include:

- Proactive Borrower Engagement — User-friendly, secure portals enabling real-time document submission, hardship reporting, and workout option tracking.

- Data-Driven Insights — Predictive analytics models that flag at-risk borrowers early, allowing targeted and compliant outreach.

- Preservation and Inspections — Timely property condition assessments to safeguard collateral value from the outset.

- Valuations and Equity Assessment — Fast broker price opinions (BPOs), appraisals, and AVMs to assess the feasibility of modifications, refinances, or short sales.

- Short Sale / Deed-in-Lieu Acceleration — Automated workflows for faster approvals and closings.

- REO Efficiency — Nationwide agent networks, centralized asset tracking, marketing resources, and coordinated closing support to shorten disposition timelines.

Quantitative Impact of Timing on Outcomes: Loss mitigation effectiveness is highly time sensitive. Interventions in the 0–90/120-day window consistently produce the strongest cure and retention results because borrower hardship is typically less severe, and regulatory options remain most flexible. Even successful modifications carry re-defaul trisk; historical OCC data have shown approximately 25% or higher rates of 60+day delinquency within six months post-modification in certain periods, though recent emphasis on combination modifications aims to improve sustainability.

Progression to REO generates substantial incremental expenses. With traditional REO inventory averaging 897 days, prorated holding costs (taxes, insurance, maintenance, utilities, and security) can reach 8–12% of property value annually, compounded by disposition fees of 5–7.5%. Successful upstream mitigation avoids these entirely while delivering better borrower and investor outcomes.

Bundling complementary services such as predictive analytics with early valuations and preservation supports flexible delivery models including subscriptions andcomprehensive default management outsourcing.

Some servicers and private investors have also benefited from selective REO strategies that allow internal or partner-led marketing of certain assets before transfer to FHA or GSE programs, reducing administrative overhead and net loss severity.

These data-supported upstream strategies consistently enhance cure rates, compress expenses, and improve recoveries across portfolios.

4. Conclusion: Partnering for Resilience and Recovery

In the 2026 environment of normalizing yet elevated foreclosure activity, organizations that combine rigorous regulatory compliance with technology-enabled early-cycle engagement gain a clear competitive edge. Integrated platforms that span the entire delinquency-to-disposition lifecycle from initial outreach and predictive analytics through streamlined mitigation and efficient REOdisposition and liquidation.

Nationwide Property & Appraisal Services (NPAS), U.S. Real Estate Services (USRES), and RES.NET collectively provide a unified ecosystem of valuation services, borrower engagement portals, property preservation solutions, loss-mitigationtechnology, and nationwide disposition expertise. These capabilities arespecifically aligned with current market conditions and regulatory demands, empowering servicers and investors to achieve stronger, more resilient results.

Organizations interested in strengthening early intervention capabilities and optimizing asset recovery are encouraged to contact the team to discuss tailored implementation approaches.

References

- ATTOM Data Solutions. (2025–2026). U.S. Foreclosure Market Reports (Year-End 2025 and January 2026).

- Auction.com / REI-INK. (2025). 2025 Disposition Strategy Report.

- Consumer Financial Protection Bureau. Regulation X, 12 CFR §1024.41.

- Office of the Comptroller of the Currency (OCC). Mortgage Metrics Reports (2025).

- California Assembly Bill 2424 (effective January 1, 2025) and related Civil Code provisions.

Disclaimer: This white paper is for informational and educational purposes only and does not constitute legal, financial, accounting, or professional advice. Market data, timelines, statutes, and regulatory interpretations are subject to change. Servicers, lenders, andinvestors should consult current official sources and qualified professionals for advice specific to their situation. All statistics are attributed to the cited sources as of their respective publication dates.